Introduction

Over-collateralisation is a powerful mechanism for allowing peer-to-peer (P2P) or peer-to-pool (P2P) lending in decentralised finance (DeFi). Lenders require borrowers to deposit more value in collateral than they take out in loans. This requirement helps ensure that there is always an incentive for borrowers to repay their loans. Where and how collateral is deposited can have a major impact on the capital efficiency of lending protocols. There are two main approaches protocols use for holding collateral in DeFi.

Escrowed collateral

The simplest way to construct an over-collateralised position is for the borrower to place their collateral in escrow for the duration of the loan. Being in escrow means that the borrower’s collateral is simply held aside by a smart contract and remains untouched for the duration of a loan.

Escrowing collateral is beneficial for the borrower, because it means they can repay their loan and release their collateral at any time of their choosing. It is also beneficial for lenders, because it means the collateral is always available to liquidators to pay down loans in the event that over-collateralisation is threatened by price moves or the accrual of too much interest. However, escrowing collateral is also capital inefficient, because assets used as collateral are not being used productively whilst being held in escrow and therefore earn borrowers no interest.

Examples

In its simplest form, escrowed collateral is used to create collateral-liability pairs. A single escrowed collateral A is used to borrow a single liability asset B.

This model was pioneered in Kashi (a Sushi-based lending protocol) and has been replicated more recently inside Frax Lend and Morpho Blue. It benefits from simplicity, but fragments liquidity for both lenders and borrowers. Lenders of B might have to choose between multiple different B vaults. Borrowers of B similarly need to carefully consider which vaults to borrow from. As liquidity is fragmented, interest rates become more volatile, leading to less predictable outcomes for both lenders and borrowers.

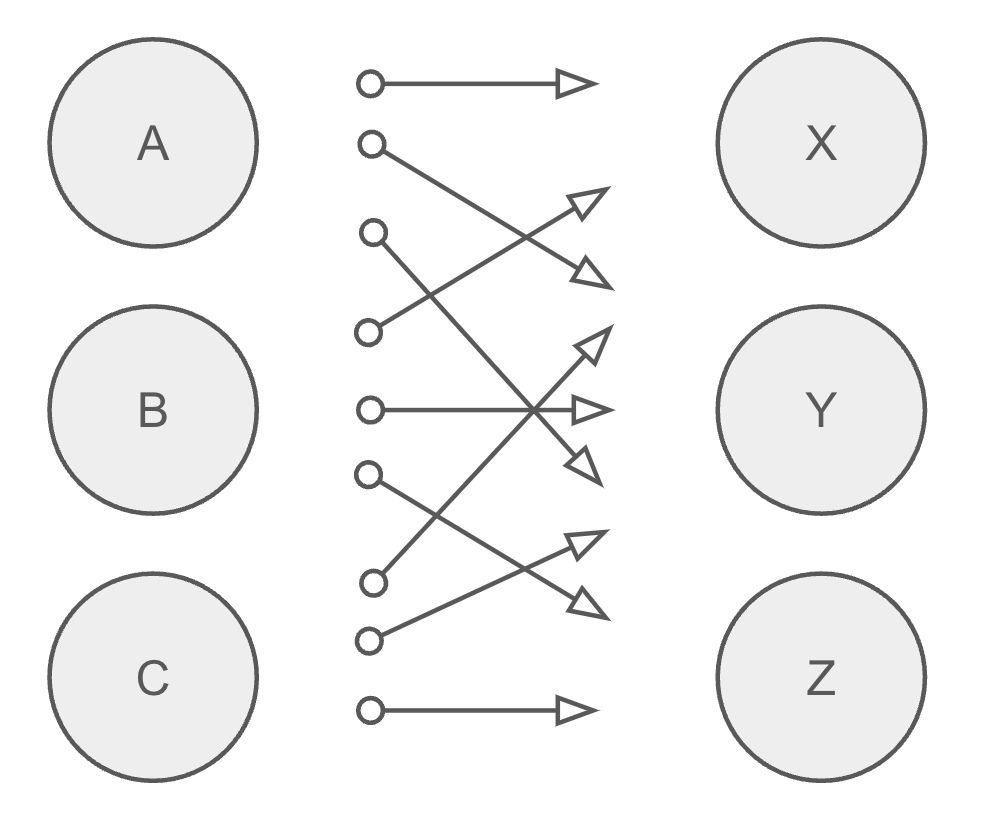

A more capital efficient version of the escrowed collateral model is used in Compound v3, where multiple escrow assets A, B, C, and so on, are used to borrow a single asset X.

This model helps reduce liquidity fragmentation, because depositors of X can earn yield from a variety of different types of collateral users at the same time. They no longer have to disperse their assets in different proportions among a range of different isolated pairs. Nevertheless, each escrowed collateral asset is still associated with only a single liability asset. This means that someone using collateral A to borrow X and Y must constantly rebalance their collateral assets between different vaults.

Thanks to its modular architecture, this restriction is relaxed inside Euler v2, allowing each liability asset to connect to multiple escrowed collateral assets, and each escrowed collateral asset to connect to multiple liability assets.

This model helps further reduce liquidity fragmentation, because users of collateral A can now borrow multiple assets using a single pool of collateral, without needing to add collateral to multiple fragmented clusters.

Collateral rehypothecation

To increase the capital efficiency of lending further, some lending protocols allow for collateral rehypothecation. What this means is that collateral is allowed to be loaned out at the same time as it is being used as collateral.

Lending collateral is often an attractive option for borrowers, because it allows them to earn yield on their collateral, lowering their net borrowing costs. In turn, this can stimulate further demand for borrowing assets, ultimately benefiting the lenders of other types of assets. Earning yield on collateral also enables novel types of trades, such as so-called ‘basis’ or ‘cash and carry’ trades.

Whilst collateral rehypothecation increases capital efficiency, it inevitably comes with trade-offs. If collateral is being loaned out, then there are times when it won’t be available for borrowers or liquidators to withdraw. Ultimately this means that lenders lending to rehypothecated collateral are taking on board greater risk than those lending to escrowed collateral, all else being equal.

Examples

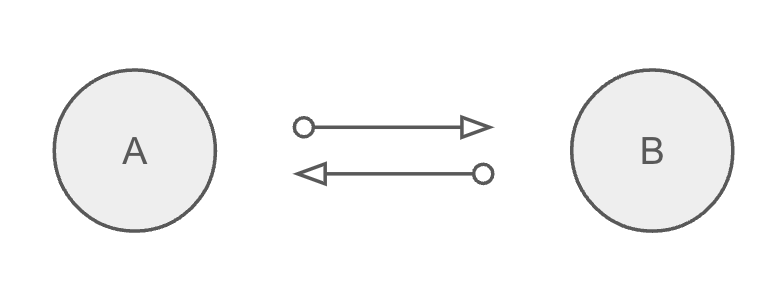

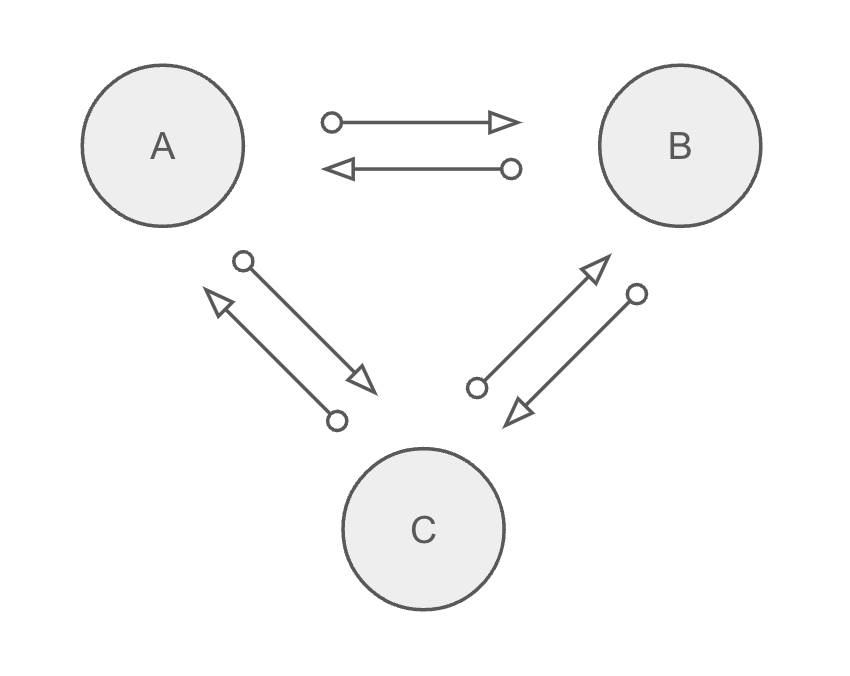

Like with escrowed collateral, the simplest form of collateral rehypothecation can be constructed with just two assets. A collateral asset A is used to borrow a single liability asset B, and vice versa (the arrows are now bi-directional).

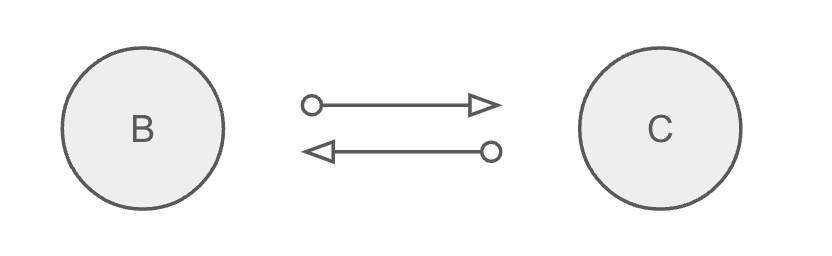

This model was pioneered in Silo. It benefits both from its simplicity and its ability to isolate risk whilst providing a more permissive environment for lending and borrowing. It isolates risk because a particular rehypothecated pair of assets can fail, causing losses to users of those assets, without causing broader system damage to all other pairs. It is more permissive for lending and borrowing because it allows more exotic assets to be used as collateral than other models of lending. To understand why, consider adding another pair of assets B and C to the pair above.

Note that in this scenario, users can not only borrow A using B, B using A, B using C, and C using B, but also A using C, and C using A. That’s because this model enables vaults to be chained together. A person using A as collateral can borrow C by first borrowing B, and then using that as collateral to borrow C.

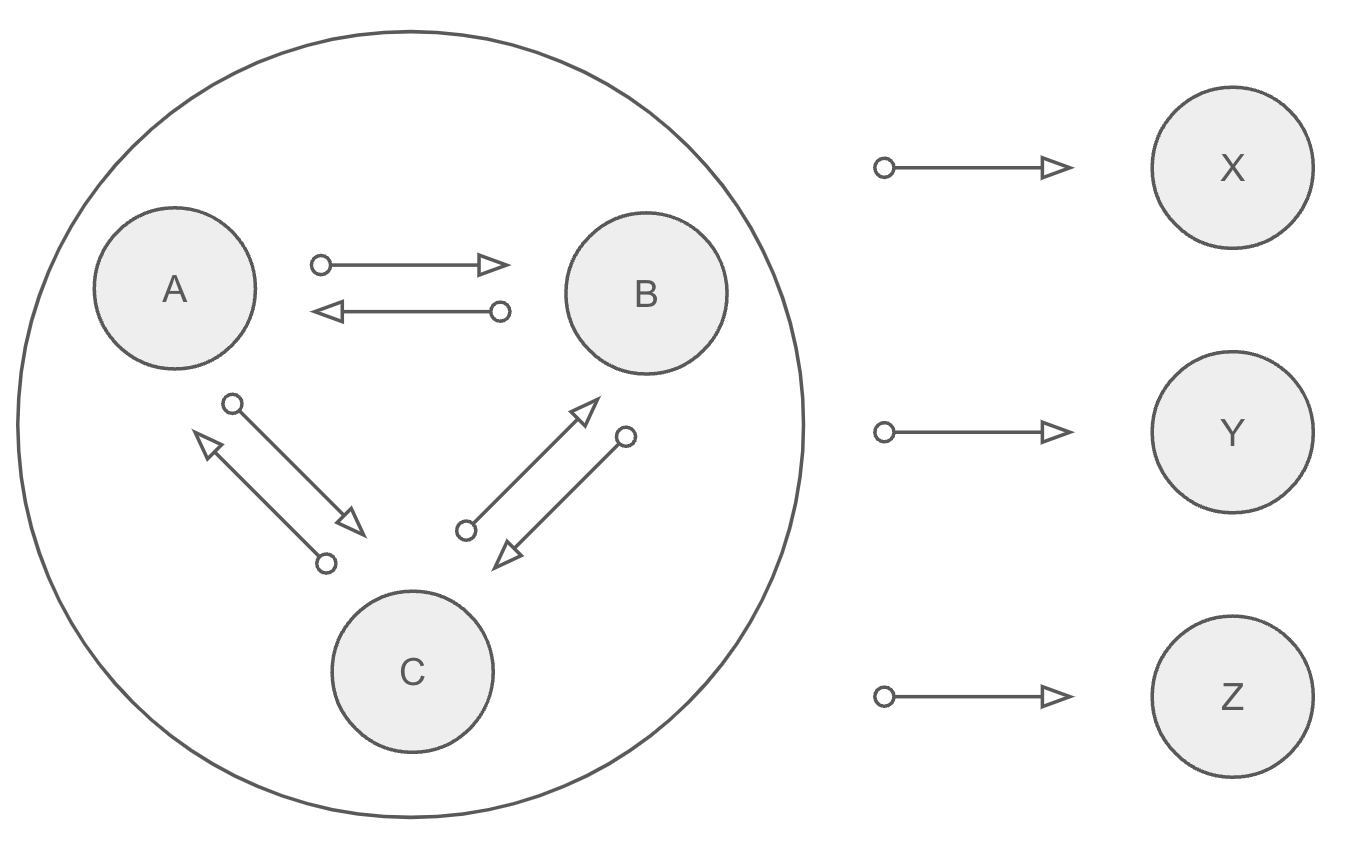

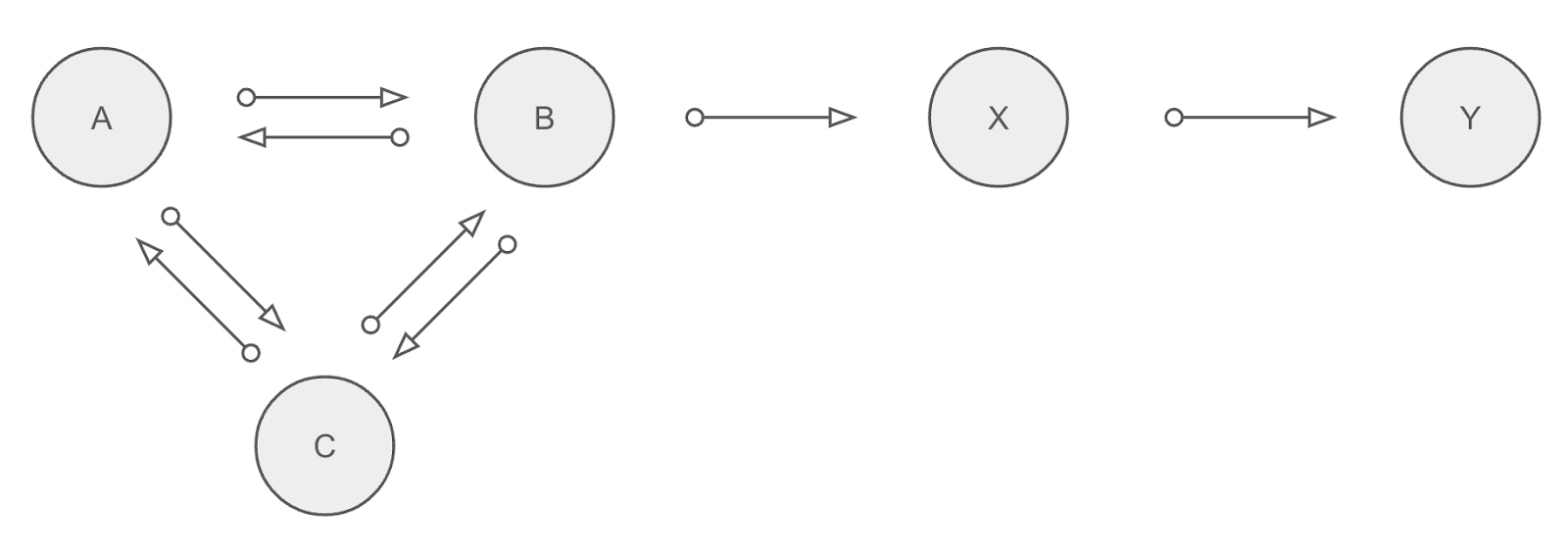

Whilst simple pairs offer many advantages, there is nothing stopping more assets being added into the mix to create what I call ‘clusters’ of collateral assets. This approach is inherent to the design of monolithic lending protocols like Compound v2, Aave v2 and v3, and Euler v1.

In those protocols, there is typically a cluster of collateral assets, A, B, C, and so on, each of which can be used to borrow one another in addition to a set of non-collateral assets, X, Y, Z, and so on.

This model is arguably the most capital efficient of all lending protocol designs. It is not without its limitations though.

Perhaps the biggest challenge with this model is that the entire system is only as strong as its weakest collateral asset. In the event borrowers fail to repay loans of asset C, loans of all other assets A, B, X, Y, Z, and so on, also become at risk of never being repaid. For this reason, collateral clusters inside monolithic lending protocols tend to be restricted to only the most liquid and least volatile assets.

Euler v2 helps solve this challenge by allowing users to create their own collateral clusters of 2 or more assets and to connect them to other individual vaults or other clusters. The Euler Vault Kit (EVK) can be used to extend the Silo model to 3 (or more) assets within a cluster.

Equally users could create an Aave-like monolith with a single collateral cluster. Or they can get creative and create entirely new types of networks of assets not seen in any other lending protocol today.

Chaining vaults in this way can bring a lot of additional capital efficiency, but also leads to additional risks. In the diagram above, a failure of A or C could lead to losses for lenders in far away vault Y. Lenders therefore need to not only carefully scrutinise the collateral accepted by their vault, but the entire downstream network of collateral.

Which is better out of escrowed collateral vs collateral rehypothecation?

The simple answer is that, like everything in financial markets, there is no free lunch. Escrowed collateral and rehypothecated collateral both have significant trade-offs, in terms of both risk and capital efficiency. Which solution prospers in a particular context depends on use-cases, market conditions, user preferences, and the assets involved.

Borrowers taking out short term loans likely will not be sensitive to net borrowing costs and may prefer to use escrowed collateral to ensure that they can close out positions at a time of their choosing.

Borrowers taking out longer term loans may be more sensitive to net borrowing costs and may prefer to find opportunities to earn yield on their collateral. In some cases, the net cost of borrowing can even turn out to be positive, allowing opportunities for positive returns from borrowing through so-called ‘cash and carry’ trades.

Lenders will often prefer for collateral to be escrowed from a risk standpoint, but prefer the extra demand that comes from allowing for collateral to be rehypothecated from a reward standpoint. Ultimately their preferences will therefore be based on risk/reward preferences and an assessment of how to maximise risk-adjusted returns in any given context.

Modularity powers innovation

With its modular design Euler v2 is unique among lending protocols in its ability to offer vault creators and users the flexibility to choose the solution that works best for them. Whether it is simple Morpho Blue pairs, rehypothecated Silo pairs, or more complex constructions like Aave v3, anything is possible with the Euler Vault Kit.

This content is brought to you by Euler Labs, which wants you to know a few important things.

This piece is provided by Euler Labs Ltd. for informational purposes only and should not be interpreted as investment, tax, legal, insurance, or business advice. Euler Labs Ltd. and The Euler Foundation are independent entities.

Neither Euler Labs Ltd., The Euler Foundation, nor any of their owners, members, directors, officers, employees, agents, independent contractors, or affiliates are registered as an investment advisor, broker-dealer, futures commission merchant, or commodity trading advisor or are members of any self-regulatory organization.

The information provided herein is not intended to be, and should not be construed in any manner whatsoever, as personalized advice or advice tailored to the needs of any specific person. Nothing on the Website should be construed as an offer to sell, a solicitation of an offer to buy, or a recommendation for any asset or transaction.

This post reflects the current opinions of the authors and is not made on behalf of Euler Labs, The Euler Foundation, or their affiliates and does not necessarily reflect the opinions of Euler Labs, The Euler Foundation, their affiliates, or individuals associated with Euler Labs or The Euler Foundation.

Euler Labs Ltd. and The Euler Foundation do not represent or speak for or on behalf of the users of Euler Finance. The commentary and opinions provided by Euler Labs Ltd. or The Euler Foundation are for general informational purposes only, are provided "AS IS," and without any warranty of any kind. To the best of our knowledge and belief, all information contained herein is accurate and reliable and has been obtained from public sources believed to be accurate and reliable at the time of publication.

The information provided is presented only as of the date published or indicated and may be superseded by subsequent events or for other reasons. As events and markets change continuously, previously published information and data may not be current and should not be relied upon.

The opinions reflected herein are subject to change without being updated.